The Foundation: What is a Credit Score?

At its core, a credit score encapsulates your credit history, amalgamating data from various sources. Ranging from 300 to 850, FICO scores, the most widely used scoring model, establish a benchmark. The higher your score, the more likely you are to secure loan approvals and favorable interest rates. This numerical representation is not arbitrary; it’s meticulously calculated based on factors such as the number of accounts, total debt levels, repayment history, and more.

In the United States, three major credit bureaus—Equifax, Experian, and TransUnion—play a pivotal role in collecting, analyzing, and disseminating consumer credit information. While FICO dominates the market, various scoring systems exist, with the FICO Score reigning supreme in financial institutions’ evaluations.

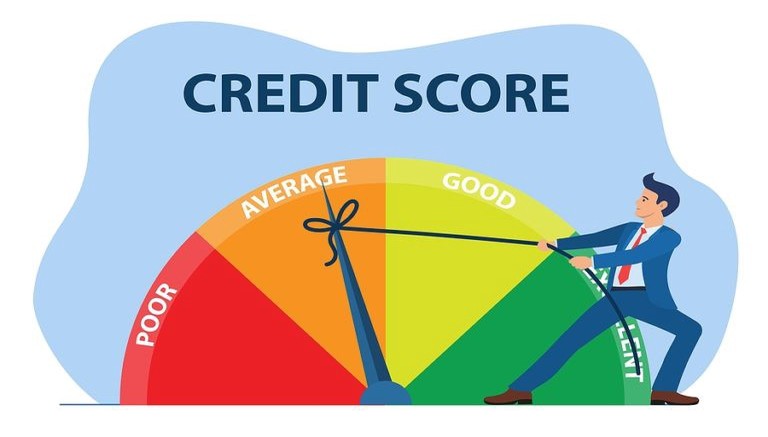

Decoding the Numbers: Understanding Credit Score Ranges

Your credit score falls into distinct categories, each influencing your financial prospects:

Excellent: 800–850

Very Good: 740–799

Good: 670–739

Fair: 580–669

Poor: 300–579

These categories provide a snapshot of your credit health, influencing lenders’ decisions and shaping your financial journey. Prospective employers may also scrutinize your credit score, and service providers might consider it when determining deposit requirements.

The Anatomy of a Credit Score

To comprehend how your credit score is derived, it’s imperative to grasp the five main factors considered by credit reporting agencies:

Payment History (35%): Timely bill payments form the bedrock of a positive credit history.

Amounts Owed (30%): Your credit utilization, or the percentage of credit used compared to your available credit, is a critical factor.

Length of Credit History (15%): A lengthier credit history is often seen as less risky, providing more data for evaluating payment patterns.

Types of Credit (10%): A diverse credit portfolio, including installment and revolving credit, signals responsible credit management.

New Credit (10%): Opening multiple new credit accounts in a short period may raise concerns about financial stability.

Credit Scores in Action: Impact on Your Financial Life

Your credit score serves as a gateway to financial opportunities. Lenders scrutinize it to determine whether to approve loans and at what interest rates. A credit score of 700 or higher is generally favorable, leading to lower interest rates. The impact extends beyond loans; it can influence your ability to secure a smartphone, cable service, or even rent an apartment.

VantageScore: A Different Perspective

While FICO dominates, VantageScore, developed collaboratively by Equifax, Experian, and TransUnion, offers an alternative credit rating. Unlike FICO, which provides three separate bureau-specific scores, VantageScore is a unified score, combining data from all three bureaus. Though FICO remains the go-to for about 90% of lenders, VantageScore provides a holistic view of an individual’s creditworthiness.

Enhancing Your Financial Profile: Tips to Improve Your Credit Score

In a dynamic financial landscape, improving your credit score is a strategic move. Consider these actionable steps:

-

Pay Your Bills on Time: Consistent on-time payments over six months can significantly boost your credit score.

Increase Your Credit Line: A higher credit limit, if used responsibly, can positively impact your credit utilization rate.

Don’t Close a Credit Card Account: Instead of closing accounts, consider keeping unused cards in a secure place. Regularly check for any fraudulent activity.

Work with Credit Repair Companies: If time is a constraint, credit repair companies can negotiate with creditors on your behalf.

Correct Errors on Your Credit Report: Regularly monitor your credit report for inaccuracies. Utilize your free annual credit report to identify and rectify errors.

The Dynamics of Credit Score Ranges

Understanding what constitutes a good credit score is pivotal. Lenders categorize scores into ranges, providing a benchmark:

Fair: 580–669

Good: 670–739

Very Good: 740–799

Excellent: 800–850

The interpretation of a “good” credit score may vary among lenders, emphasizing the importance of staying informed about your financial standing.

Behind the Scenes: Who Calculates Credit Scores?

The three major credit bureaus—Equifax, Experian, and TransUnion—collectively calculate FICO scores. While each bureau utilizes the same information, slight variations may arise due to differing calculation methods. FICO, with its widespread usage, remains the linchpin of credit scoring.

Accelerating Credit Score Improvement

For those seeking a rapid boost in their credit score, innovative services like Experian Boost offer an avenue to include additional payment information, such as rent and utilities. Leveraging a positive track record in these areas can expedite credit score enhancement.

The Finale: Navigating Your Financial Journey

In conclusion, your credit score is more than just a number; it’s a compass guiding your financial voyage. A good credit score opens doors to financial opportunities and favorable terms. By understanding the intricacies of credit scoring, taking proactive steps to enhance your credit profile, and staying abreast of technological advancements, you empower yourself to navigate the digital landscape with confidence. Whether it’s securing a loan, renting an apartment, or even landing your dream job, your credit score is a key player in shaping your financial narrative.

Instant Information: Transformative Trends in Credit Scoring

As we navigate the fast-paced digital era, the landscape of credit scoring undergoes continuous evolution. Instant information, driven by technological advancements, has become a game-changer, influencing the way credit scores are calculated, accessed, and utilized across various industries. In this dynamic continuation of our exploration, let’s delve into the current technological trends shaping credit scoring, their impact on diverse sectors, and the potential future scenarios.

The Rise of Real-Time Data

One of the most significant shifts in credit scoring is the integration of real-time data. Traditionally, credit scores were based on historical information, offering a retrospective view of an individual’s financial behavior. However, the advent of real-time data analytics allows for a more dynamic and responsive assessment. This shift is particularly evident in the utilization of alternative data sources beyond the conventional credit report.

Alternative Data and Its Implications

The expansion of alternative data sources has become a focal point in the evolution of credit scoring. Beyond the traditional metrics considered by credit bureaus, alternative data encompasses a broader spectrum of information, including:

Utility Payments: Timely payments for utilities, such as electricity and water bills, are gaining recognition as indicators of financial responsibility.

Rental Payments: Your track record of paying rent can now contribute to your credit profile, offering a more holistic view of your financial habits.

Mobile Phone and Internet Payments: As digital payments become ubiquitous, your promptness in settling mobile phone and internet bills can influence your creditworthiness.

The inclusion of such alternative data not only provides a more comprehensive assessment but also opens doors for individuals with limited or no traditional credit history.

Artificial Intelligence and Machine Learning

Artificial Intelligence (AI) and Machine Learning (ML) have ushered in a new era of credit scoring. These technologies go beyond traditional scoring models by analyzing vast datasets to identify patterns and trends. The predictive capabilities of AI and ML enable a more accurate assessment of an individual’s credit risk, allowing lenders to make informed decisions in real-time.

Blockchain Technology in Credit Scoring

Blockchain, known for its decentralized and secure nature, is making inroads into credit scoring. The use of blockchain can enhance data security and streamline the sharing of credit information among financial institutions. This decentralized approach has the potential to reduce fraud and provide individuals with more control over their credit data.

Open Banking and Credit Scoring

Open Banking initiatives, driven by the sharing of financial data between banks and third-party providers, are transforming the credit landscape. This collaborative approach allows for a more detailed analysis of an individual’s financial behavior, leading to personalized credit assessments. The seamless flow of information between financial institutions enhances accuracy and efficiency in credit scoring.

The Future of Credit Scoring: Personalization and Inclusivity

Looking ahead, the future of credit scoring is poised to be more personalized and inclusive. Technological advancements will continue to refine scoring models, tailoring them to individual financial profiles. Personalization not only ensures a fairer assessment but also enables lenders to offer more customized financial products.

Furthermore, a key focus of future credit scoring trends is inclusivity. The use of alternative data, coupled with advanced analytics, aims to bridge gaps in traditional credit evaluation, making financial opportunities accessible to a broader spectrum of individuals.

Embracing the Change: Navigating the Technological Wave

In embracing these technological trends, it’s essential for individuals to stay informed about the changing landscape of credit scoring. Regularly monitoring credit reports, understanding the impact of alternative data, and being aware of the role of AI and blockchain can empower consumers to navigate the evolving credit ecosystem with confidence.

As the digital transformation of credit scoring continues, the synergy between innovation and responsible financial practices will shape a future where access to credit is not just about numbers but reflects the diverse and dynamic financial journeys of individuals. The instant availability of information, coupled with advanced analytics, is not just a technological trend; it’s a paradigm shift that holds the potential to redefine how we perceive and interact with credit in the years to come.